Benefits of Virtual Business Credit Cards for Corporate Travel

Edward Taylor

-

Corporate travel can often create reimbursement delays, rising fraud exposure for financial teams, and overall weak oversight.

-

Many modern virtual cards let businesses apply merchant controls, granular spending limits, and trip specific restrictions.

-

International companies often benefit from better FX handling, fewer failed travel payments abroad, and easier issuance.

-

For many growing companies, virtual cards for business are more scalable and secure than relying solely on physical corporate cards.

Business travel spending can quickly become messy. Employees lose receipts, finance departments spend hours managing transactions manually, and reimbursement requests pile up. Traditional expense systems were built around static physical cards, heavy administrative oversight, and delayed reporting. However, that model doesn't work anymore, especially as companies scale, remote teams become more common, international operations arise, and travel schedules are frequent.

This is why virtual cards have become more than just a modern payment tool. When it comes to the modern corporate travel context, they act as programmable payment controls, allowing companies to manage fraud exposure, policy enforcement, employee spending, and reconciliation, all without slowing down operations.

Instead of having to issue a single shared company card with broad permissions, businesses can now create purpose specific virtual payment cards for meals, hotels, events, flights, or even individual employees. This guide will discuss the various benefits of virtual business credit cards for corporate purposes, particularly for travel.

8 Benefits of Virtual Business Credit Cards for Corporate Travel

There are 8 main benefits of virtual business credit cards for travel purposes in a corporate setting.

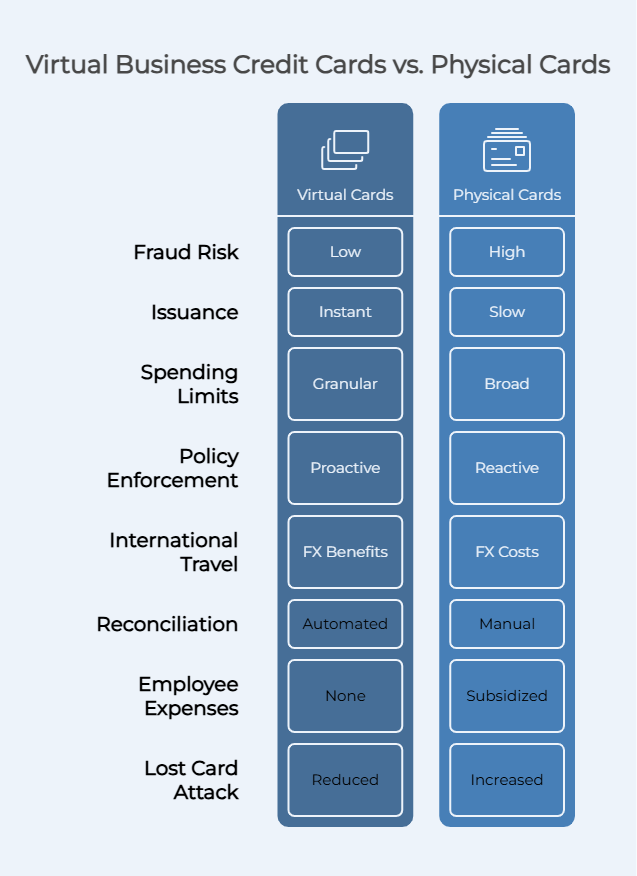

1. Fraud Containment and Reduced Fraud Risk

One of the most important operational advantages of virtual cards for business is fraud containment. The fact is that traditional physical corporate cards create broad exposure as one compromised card can potentially affect an entire department or travel program. This becomes very risky during frequent business travel, where card details are often shared repeatedly across airline systems, hotel bookings, rideshare apps, international vendors, and restaurants.

With virtual credit cards, companies are able to generate unique card numbers that are tied to a single vendor, trip, employee, or even a single booking. The benefit is that if a card is compromised, the impact is isolated to just that specific transaction or spending environment.

This drastically improves fraud prevention, as companies can issue cards with highly controlled parameters, such as merchant restrictions, date restrictions, geographic restrictions, transaction caps, one time use configurations, and department specific rules.

For example, a travel manager could create a temporary corporate virtual card that only works at approved hotel chains within a defined date range, but if the card details are leaked later, they become effectively useless.

2. Instant Issuance for Last-Minute Business Trips

Travel plans can quickly change, with flights getting rebooked, conferences appearing suddenly, and employees often requiring immediate access to approved spending tools. The fact is that traditional corporate cards are very slow in these situations because issuing new physical cards usually requires shipping delays, approval chains, and administrative processing.

On the other hand, virtual cards can be created within seconds. This greatly changes how companies manage urgent business trips. Instead of having to ask employees to use personal cards and then wait for reimbursements, finance departments can instantly issue a purpose-specific card tied directly to that traveler or itinerary.

This can create several operational advantages, including faster employee onboarding, reduced reimbursement requests, less employee frustration, cleaner accounting workflows, and better spending oversight. For growing companies, this flexibility is critical, as a scaling startup may suddenly need to issue secure travel payments to sales teams, contractors, or executives in multiple countries without being able to wait for bank logistics.

3. Granular Spending Limits and Card Controls

Traditional shared company cards create a large visibility problem. The issue is that once an employee has access to the card, spending authority generally becomes far broader than intended. This then forces accounting departments to clean up problems later instead of preventing them in the first place.

This is where virtual cards change the control model. Companies are able to create highly customizable spending limits that are tied to individual employees, projects, departments, and specific transaction categories. This means that rather than having to review expenses after the fact, businesses are able to proactively define what is allowed before the card is ever used.

Modern cards for businesses often support daily limits, per transaction limits, merchant restrictions, geographic restrictions, expiration controls, department budgets, and MCC restrictions. For example, a company may issue a virtual card exclusively for airfare with a strict cap, while another card only works for approved hotel chains. This level of control greatly reduces unauthorized business spending and overall simplifies internal approvals.

4. T&E Policy Enforcement Without Constant Oversight

Expense policy enforcement is very reactive. Employees spend first and then accounting departments review receipts later and determine whether the purchase complied with company rules. This process creates a lot of delayed approvals, significant manual work, and unnecessary friction.

That said, with virtual cards, companies shift to more proactive policy enforcement. Rather than auditing every expense manually, businesses are able to configure rules directly to the payment method itself. This lets organizations restrict spending outside approved travel categories or vendor types.

Some examples of this include restricting alcohol purchases, blocking luxury hotel bookings, preventing non approved airline purchases, limiting rideshare spending, and disabling ATM access. This reduces the reliance on employee compliance alone and also reduces the burden on accounting teams, which would otherwise spend large amounts of time reviewing expense reports, correcting coding issues caused by human error, and resolving disputes.

In a larger corporate travel context, this automation is also incredibly useful as companies that manage hundreds of monthly trips can't realistically audit every transaction manually without significant operational overhead.

5. FX and Multi-Currency Benefits for International Travel

International travel introduces another layer of complexity into corporate spending, as exchange rates fluctuate constantly, card acceptance varies by country, and many traditional banking products generate unnecessary FX costs or failed transactions abroad.

This is why virtual cards for businesses are important. The reason is that modern providers increasingly support local currency settlement, multi currency balances, region specific card routing, international vendor compatibility, and dynamic FX management. For companies that have to manage global teams or deal with recurring international travel, these capabilities reduce overall failed payments and improve traveler reliability.

Some issuers may also provide US BIN Visa or Mastercard products, even for non-US companies. This is important because many US airlines, vendors, ad platforms, and booking systems process US-issued cards more reliably than foreign prepaid products. Companies can also create region specific virtual cards for employees that are traveling internationally, therefore reducing exposure for the broader corporate account.

This is very useful for international conferences, multi country operations, and global contractor payments. Instead of relying on employees to cover their expenses using their own personal cards, businesses can issue approved virtual payment cards directly for that trip.

6. Better Reconciliation and Automated Reconciliation

Regular travel expense management can create massive reconciliation problems. Employees often submit receipts late, accounting departments have to manually match expenses to statements, and there's often missing documentation.

This is actually one of the biggest reasons why many organizations choose virtual cards instead. This is because each card can be tied directly to a specific employee, department, trip, vendor, or project. This structure improves transaction data quality as every payment already contains contextual information before reconciliation ever begins.

Modern platforms often also support accounting exports, accounting software syncing, ERP integrations, department tagging, real time reporting, and more. Many systems also allow for project codes and travel metadata to be attached directly at issuance.

This not only improves automatic reconciliation, but also downstream reporting accuracy. Instead of having to rely on employees to manually explain their purchases, transactions are automatically matched to predefined departments, budgets, or trip records. This reduces overall receipt chasing, coding errors, manual reconciliation, approval delays, and administrative overhead.

7. Eliminating Employee Out-of-Pocket Expenses

One of the problems that nobody appreciates in corporate travel is how often employees have to subsidize company operations temporarily. Many businesses expect staff to cover flights, meals, hotels, and ride share expenses using their own personal cards, then wait days or weeks for reimbursement.

This creates frustration for employees, especially for frequent travelers or junior staff carrying large balances across recurring business trips. Using virtual business credit cards changes this completely. Instead of employees having to front costs personally, finance departments are able to issue trip-specific cards in advance. Employees receive approved spending access right away without needing to take on temporary financial strain.

This creates many operational advantages, including increased employee satisfaction, cleaner accounting, better compliance, reduced reimbursement fraud, fewer reimbursement disputes, and lower administrative burden. It also helps improve visibility into real time business expenses rather than having to rely on delayed reimbursement workflows.

8. Reduced Lost-Card Attack Surface Compared to Physical Cards

Stolen or lost physical cards are one of the biggest operational risks in travel spending. Employees can lose wallets, cards get cloned, hotel staff accidentally record details, and more. Shared team cards circulate between multiple travelers as well.

These scenarios all create unnecessary exposure. Static card numbers are vulnerable as they are used repeatedly across multiple regions, vendors, and payment environments.

On the other hand, virtual cards greatly reduce this attack surface, as companies can issue cards tied directly to individual vendors, limited timeframes, specific transaction types, single trips, and defined windows. Once the trip ends, the card is frozen or expires automatically. This creates much stronger operational containment rather than having to rely on long-lived physical corporate cards with broad permissions.

Physical vs. Virtual Corporate Cards for Business Travel

| Category | Physical Corporate Cards | Virtual Cards |

|---|---|---|

| Issuance Speed | Days to weeks | Instant |

| Replacement Process | Requires shipping | Immediate reissue |

| Fraud Exposure | Broad shared exposure | Isolated per-card risk |

| Spend Controls | Limited | Granular programmable controls |

| International Flexibility | Moderate | Strong |

| Employee Reimbursements | Common | Reduced |

| Reconciliation | Often manual | More automated |

| Mobile Wallet Support | Sometimes | Common |

| Vendor-Specific Issuance | Difficult | Easy |

For most organizations, shifting from physical cards to virtual cards for business is not as much about replacing plastic entirely and more about improving operational control. The fact is that traditional card programs are designed around static spending and delayed reconciliation. Modern travel programs however require faster approvals, flexibility, and stronger security, along with cleaner transaction data.

This doesn't mean companies should completely abandon physical cards, as some companies may still need them for legacy systems, edge cases, or travelers who frequently require fallback payment options. With that being said, for most recurring business travel, virtual cards create substantially better visibility, stronger fraud protection, and less administrative overhead.

How Per-Trip Virtual Card Issuance Works in Practice

For an example, let's imagine a sales manager attending a three-day conference in Los Angeles. Instead of having to give this employee access to broad company card details, the finance department can create several trip specific virtual cards in advance.

The company can issue a card for airfare, another for hotel bookings, another for meals and local transportation, and an emergency backup card. Each of these cards then includes defined spending limits, approved vendor categories, trip specific expiration dates, geographic restrictions, and even department level tracking.

The hotel card will only work with approved hotel chains during the approved travel window, the meal card has a capped daily allowance, and the emergency card is inactive unless approved manually. This kind of structure improves oversight while reducing unnecessary employee friction.

It also reduces the operational problems that can be caused by lost receipts, shared cards, incorrect coding, delayed reporting, or unauthorized purchases. When they are integrated properly, virtual card transactions feed directly into ERP and expense systems with predefined categorization already attached.

How to Evaluate Virtual Card Providers for Corporate Travel

Here's how to evaluate various virtual cards for corporate travel.

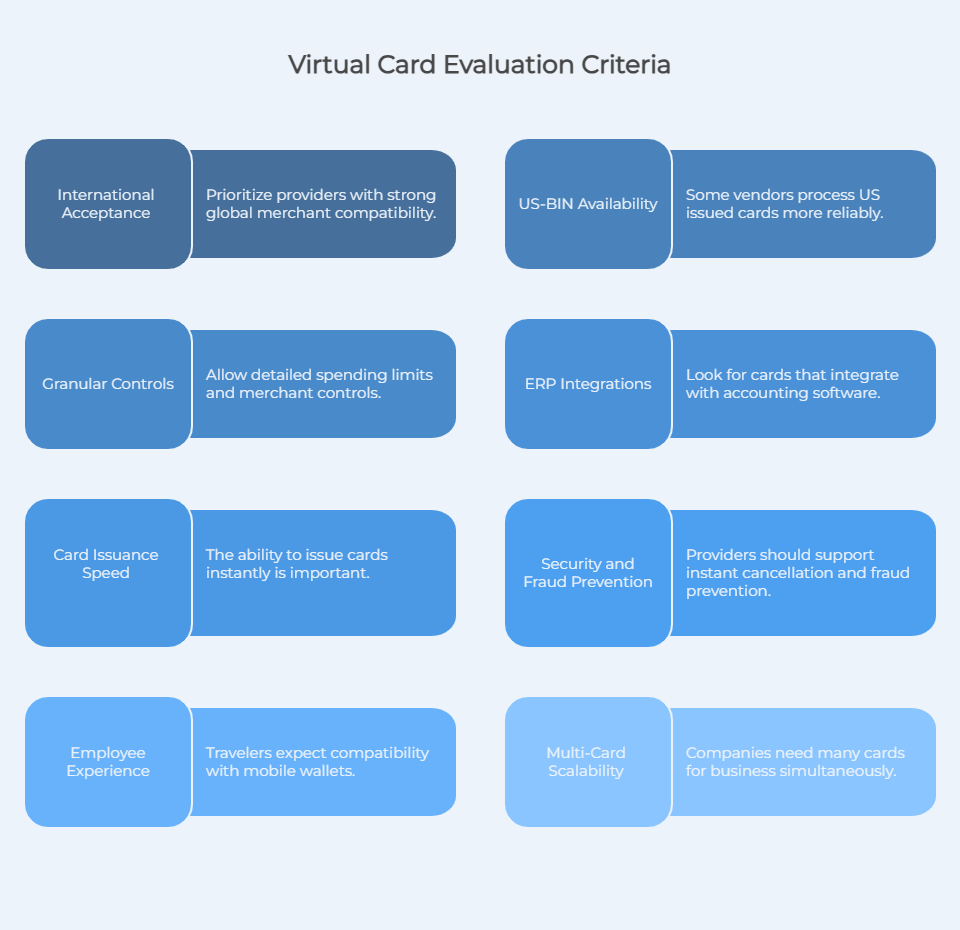

International Acceptance

Companies that manage frequent international travel have to prioritize providers with strong hotel, airline, and global merchant compatibility.

US-BIN Availability

Some vendors process US-issued cards more reliably than foreign prepaid products. This matters heavily for various subscriptions, travel booking systems, and airlines.

Granular Controls and Spending Limits

Good providers allow companies to apply detailed spending limits, trip-level restrictions directly at issuance, and merchant controls.

ERP and Expense Integrations

Look for cards that feature integrations with major accounting software, expense management platforms, and ERP systems.

Card Issuance Speed

For businesses, especially last-minute scenarios, the ability to issue cards instantly is very important.

Security and Fraud Prevention

Providers should support instant cancellation, dynamic card freezing, merchant restrictions, and strong visibility into transaction details. Providers like Halocard also featured 3D Secure Authentication for an added layer of protection.

Employee Experience and Mobile Wallets

Travelers often expect compatibility with mobile wallets, including Google Pay and Apple Pay.

Multi-Card Scalability

Some virtual card providers are better at large scale issuance than others. Companies that manage regional teams, contractors, or multiple departments need many cards for business simultaneously without having any operational bottlenecks.

Virtual Card Providers for Corporate Travel: How They Compare

| Provider | Card Type | Network | International | US-BIN | FX Fee | Per-Trip Cards | Best For |

|---|---|---|---|---|---|---|---|

| Halocard | Secured Visa credit card | Visa | Yes | Yes | 1.5% non-USD | Yes | International travel and US merchant acceptance |

| Ramp | Corporate cards | Visa | Moderate | Yes | Limited | Yes | US startups |

| Brex | Corporate cards | Mastercard | Moderate | Yes | Limited | Yes | Venture-backed companies |

| Wise | Virtual cards | Visa/Mastercard | Strong | No | Low FX | Moderate | Multi-currency spending |

| Revolut Business | Virtual cards | Visa/Mastercard | Strong | Partial | Low FX | Yes | International teams |

Frequently Asked Questions

What Are Virtual Credit Cards in a Corporate Travel Context?

In a corporate travel context, virtual credit cards are digitally generated payment cards that are approved for company spending without requiring permanent plastic cards.

How Do Virtual Cards Improve T&E Policy Enforcement?

Virtual cards improve this kind of enforcement because they allow businesses to apply merchant restrictions, trip dates, spending rules, and approval logic right to the payment method itself.

Can Virtual Cards Handle Hotel Pre-Authorization Holds?

Yes, virtual cards can handle hotel pre-authorization holds, although some hotels still prefer backup physical cards at check-in.

Are Virtual Cards Safer Than Physical Corporate Cards?

Generally speaking, yes, virtual cards are safer than physical corporate cards, as they reduce long-term exposure by isolating payment credentials to specific vendors, trips, and transactions.

Can Companies Use Virtual Cards for International Travel?

Yes, many providers allow for their virtual cards to be used for international travel, as they support global issuance, FX management, and multi currency acceptance.

Do Virtual Cards Integrate With Expense Platforms and Accounts Payable Systems?

Yes, many providers integrate directly with ERP, expense systems, and accounting to improve overall reporting and reconciliation.

Why Do Some Employees Dislike Virtual Cards?

Some travelers may prefer physical cards because certain regions, vendors, or offline scenarios may require plastic fallbacks.

Can Companies Issue Multiple Corporate Cards for the Same Trip?

Yes, many modern platforms allow for finance departments to issue multiple trip-specific virtual cards that are tied directly to employees, vendors, or budgets.

Sources

-

Covington Travel. 5 Benefits of Virtual Cards for Managing Business Travel Spend

-

Concur. Getting the Most Out of Virtual Cards for Business | SAP Concur Canada

-

BCD Travel. Virtual Cards: Make Business Travel Payments Easier

-

WEX. 7 advantages to virtual cards for your B2B payment needs | WEX Inc.

-

Reddit. Do you use your business card or your personal card for business travel expenses? : r/CreditCards

-

Airwallex. 10 Pros & Cons of Virtual Cards in 2024 | Airwallex CA

-

Navan. Benefits of Virtual Credit Cards for Corporate Travel

-

Float Financial. Top Five Use Cases for Virtual Cards in Canadian Businesses - Float

-

Halocard. Instant, Private & Secure Virtual Cards | Halocard

-

Brex. Brex: The Modern Finance Software Platform | Spend Smarter

-

Brex. Corporate credit cards for startups and growing businesses

-

Wise. Virtual Card | Create your Wise Virtual Debit Card - Wise

-

Revolut. Business Account | Manage Your Finances | Revolut Business

Sources checked on May 20, 2026.

*Please see Halocard's Terms of Service or Pricing for the most up to date pricing and fee information. This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Halocard LLC or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Halocard Virtual Cards

Instant approval

Create your first card in under 5 minutes.

Private purchases

Purchases never appear on your bank account.

Powered by Visa

Accepted at 175M+ merchants globally.

3 steps to create your virtual credit card

1. Sign-up with a phone

Sign up from your browser. No app download needed.

2. Quick identity check

Verify you're a real person in less than 3 minutes. No US residency required.

3. Add funds to your account

Use stablecoins, debit/credit card, or bank transfer (1%).

Your virtual card is ready.

That's it! Your virtual cards can now be used for online and in-person purchases anywhere in the world where Visa is accepted.