-

Virtual cards are best for agencies, SMBs, remote teams, and SaaS-heavy companies, as well as businesses that manage large volumes of online payments and recurring vendor spend.

-

The biggest problem that virtual cards solve is the uncontrolled spending that is tied to shared physical card usage, exposure to fraud or failed reconciliation, and poor visibility.

-

This guide compares Halocard, Airwallex, Ramp, Brex, Extend, and WEX for subscriptions, ad spend, employee purchasing, and business travel.

-

For those operating internationally, a US-issued virtual credit card is usually the best option in terms of strong merchant acceptance, particularly when compared to regional debit cards or prepaid alternatives.

Virtual Cards for Business - Quick Comparison

| Provider | Type | Monthly Fee | Funding | Cards per Month | Acceptance | Best For |

|---|---|---|---|---|---|---|

| Halocard | US-issued secured Visa credit card | From $12/month | Stablecoins, ACH, debit/credit funding | Tier-based | Strong US acceptance through secured Visa credit card structure | International operators, SaaS, ad spend |

| Airwallex | Multi-currency business spend platform | Free plan available; paid plans from $12/user/month + platform fees | Business wallet and bank account funding | Unlimited cards | Strong international acceptance | Global SMBs and remote teams |

| Ramp | Corporate spend and automation platform | Free plan available; Plus from $15/user/month + platform fees | Linked bank account | Unlimited virtual cards | Strong US and Canadian acceptance | Finance automation and startups |

| Brex | Corporate spend management platform | Free Essentials plan; Premium from $12/user/month | Treasury and corporate accounts | Unlimited global cards | Accepted in 210+ countries | Scaling and venture-backed companies |

| Extend | Virtual card management platform | Free Starter plan; Pro starts at $119.90/month | Existing Mastercard accounts | Up to 100–500 cards/month depending on plan | Depends on issuer | Existing corporate card users |

| WEX | Enterprise and fleet payment platform | Custom pricing | Enterprise billing and payment structure | Enterprise scale | Strong for fleet/travel categories | Logistics and enterprise travel |

Top Virtual Cards for Businesses in 2026

Here are the top virtual cards for businesses in 2026.

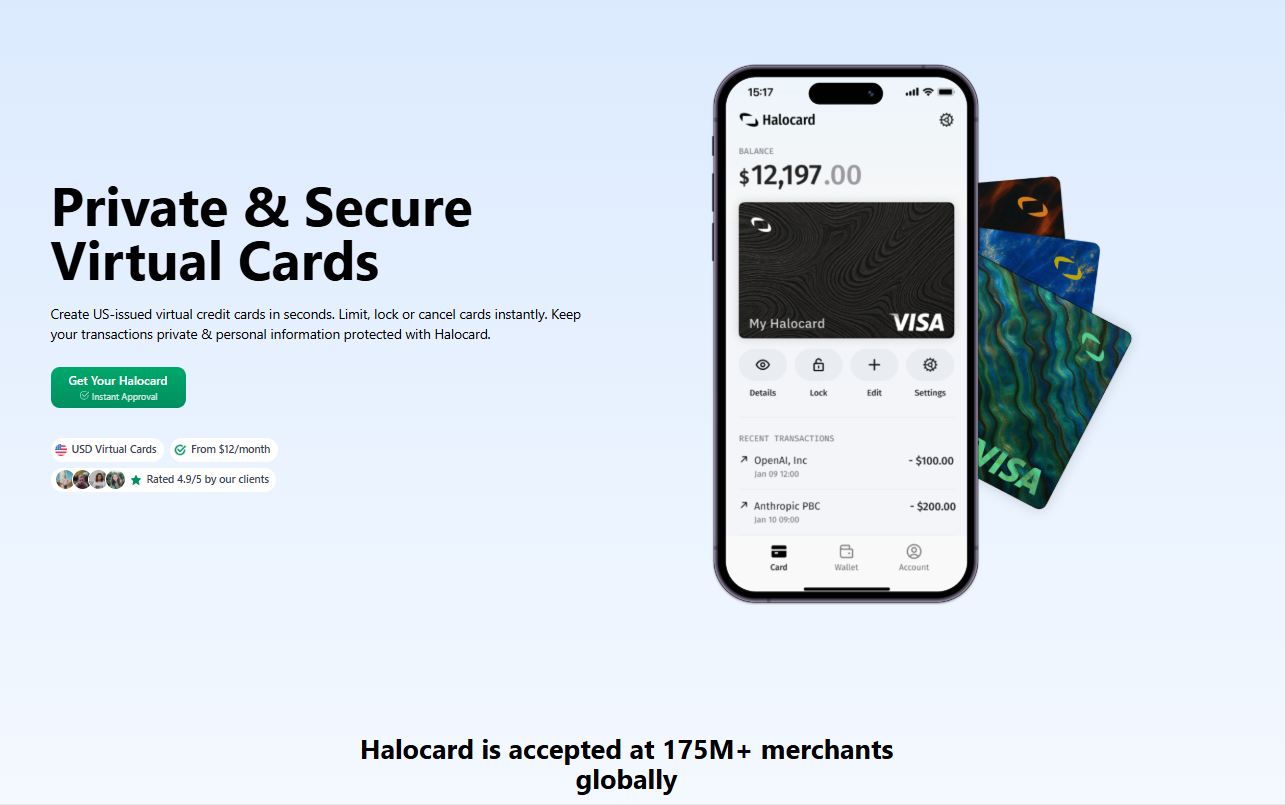

Halocard

Halocard provides its users with US-issued virtual credit cards through secured funding. Businesses can preload funds, create multiple virtual cards, and then assign them to subscriptions, employees, vendors, or ad accounts. Every single card includes dedicated card details, usage controls, and billing settings.

Costs & Fees

-

Plans start from approximately $12/month

-

Stablecoin funding is free

-

Debit and credit card funding includes processing fees

-

1.5% FX fee applies to non-USD transactions

-

USD transactions carry 0% FX fees

Spending Limits & Usage Restrictions

Businesses are able to apply customizable spending limits, expiration controls, and merchant restrictions. Cards can also be limited by frequency, transaction amount, and monthly budget.

Key Advantages

-

Strong US merchant acceptance compared to many regional virtual debit cards

-

Supports Apple Pay, Google Pay, and other mobile wallets

-

Instant card locking and cancellation

-

Useful for SaaS subscriptions, ad platforms, and vendor payments

-

Good fit for international users without a US SSN

Specific Drawbacks

-

Requires prepaid funding rather than revolving credit

-

FX fees apply on non-USD spend

-

Limited physical card functionality compared to enterprise banking platforms

Who It's For

Halocard is best for agencies, ad buyers, SaaS heavy companies, remote businesses, and international founders who need reliable US billing acceptance.

Why Choose Over Others

Halocard behaves more like a US-issued virtual credit card product during merchant authorization checks, unlike many regional virtual debit products. This improves approval rates for US platforms and advertising networks.

Airwallex

Airwallex features global accounts, virtual cards, FX management, and spend controls in a single international finance platform. Businesses are able to create cards for employees, subscriptions, departments, and recurring business payments.

Costs & Fees

-

Explore plan starts at $0/user/month

-

Grow plan starts at $12/user/month plus platform fees

-

Accelerate plan uses custom pricing

-

FX conversion fees start around 0.5% above interbank rates for major currencies

-

SWIFT transfers typically cost $15–$25 per transfer

Spending Limits & Usage Restrictions

Admins are able to freeze cards instantly, create card specific controls, and apply spending rules that are tied to departments or vendors.

Key Advantages

-

Unlimited multi-currency corporate cards

-

Strong support for international business travel and FX management

-

Integrates with QuickBooks, Xero, NetSuite, and Dynamics 365

-

Supports Apple Pay, Google Pay, and global card issuance

-

Strong automation for accounts payable and expense workflows

Specific Drawbacks

-

Platform pricing becomes more complex as teams scale

-

Some US merchants still prefer domestic-issued cards

-

Certain advanced features are locked behind higher-tier plans

Who It's For

Airwallex is best for international SMBs, companies handling cross-border online payments, and distributed teams.

Why Choose Over Others

Someone might choose this service over others when businesses require combined FX infrastructure, scalable virtual card payments, and global accounts, all in a single platform.

Ramp

Ramp combines expense management, reimbursements, corporate cards, bill pay, and AI-powered finance automation in one system.

Costs & Fees

-

Free plan starts at $0/user/month

-

Plus plan starts at $15/user/month plus platform fees

-

Includes unlimited CAD and USD virtual cards

Spending Limits & Usage Restrictions

Finance teams are able to create separate cards, approval workflows, merchant restrictions, and automatic compliance policies.

Key Advantages

-

Strong automation for expense management systems

-

AI-powered receipt matching and invoice extraction

-

Excellent integrations with QuickBooks, Xero, NetSuite, and Sage Intacct

-

Automated approval workflows and policy enforcement

-

Strong reporting for finance teams

Specific Drawbacks

-

Primarily focused on North American businesses

-

Some features require paid tiers

-

International functionality is less flexible than Airwallex

Who It's For

Ramp is best for Canadian and US startups, finance teams, and scaling SMBs that are focused on automation.

Why Choose Over Others

Ramp is a strong platform for reducing human error, simplifying financial operations, and automating reconciliation.

Brex

Brex features a combination of global corporate cards, travel tools, reimbursements, spend management, and account automation.

Costs & Fees

-

Essentials plan starts at $0/user/month

-

Premium plan starts at $12/user/month

-

Enterprise pricing is custom

Spending Limits & Usage Restrictions

Businesses are able to assign role based policies, live budget controls tied to employee spending, and approval chains.

Key Advantages

-

Unlimited global cards accepted in 210+ countries

-

Local-currency cards available in 50+ countries

-

Strong travel and reimbursement features

-

Advanced accounting automation

-

Good support for multi-entity organizations

Specific Drawbacks

-

Best features are locked behind Premium and Enterprise plans

-

Eligibility requirements may exclude smaller businesses

-

Can feel enterprise-heavy for lean SMBs

Who It's For

Brex is best for fast-growing companies, international organizations, and venture backed startups.

Why Choose Over Others

Brex has sophisticated spend controls along with global card infrastructure, making it a good choice for international scaling.

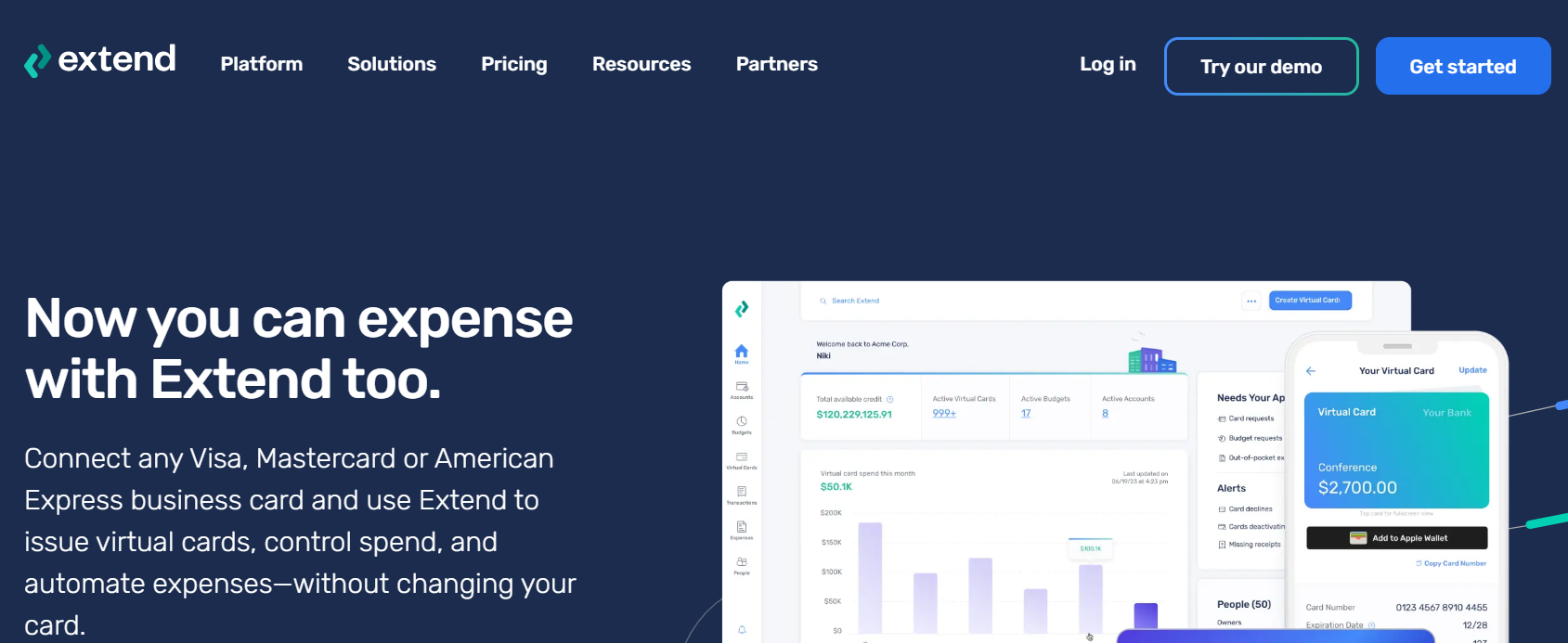

Extend

Extend is ideal as it allows businesses to generate virtual cards from existing Mastercard credit accounts instead of replacing a current card setup.

Costs & Fees

-

Starter plan is free with up to 5 users and 100 virtual cards/month

-

Pro starts at approximately $119.90/month and supports up to 500 cards/month

-

Enterprise pricing is custom

-

Pricing varies by bank partner

Spending Limits & Usage Restrictions

The capabilities depend on the connected issuer, although admins can still assign budgets, usage controls, and approval workflows.

Key Advantages

-

Works with existing Mastercard programs

-

Supports QuickBooks Online sync and reimbursements

-

Includes receipt management and budgets

-

Reduces disruption to existing finance infrastructure

-

Strong temporary card issuance controls

Specific Drawbacks

-

Features depend heavily on supported bank partners

-

Limited flexibility compared to fully integrated spend platforms

-

Card issuance volume depends on plan tier

Who It's For

Extend is ideal for businesses that are already using enterprise Mastercard accounts and want enhanced security and spending controls.

Why Choose Over Others

Extend is an ideal choice for companies who want virtual issuance without having to migrate away from their existing corporate card programs.

WEX

WEX is specifically focused on enterprise payment infrastructure for fuel management, fleets, and travel-heavy organizations.

Costs & Fees

-

Pricing is custom and depends on transaction volume, industry, and usage requirements

-

Businesses typically need to contact WEX directly for enterprise quotes

-

Enterprise implementations may include additional onboarding or integration costs

Spending Limits & Usage Restrictions

Controls can be tied to vehicles, drivers, fuel categories, and travel policies.

Key Advantages

-

Strong specialization in fleet and transportation spending

-

Useful for enterprise business travel programs

-

Detailed category controls and reporting

-

Well suited for logistics-heavy organizations

Specific Drawbacks

-

Less flexible for SaaS and startup-style purchasing

-

Enterprise onboarding may be slower than SMB-focused platforms

-

Not designed primarily for lightweight subscription management

Who It's For

WEX is best for logistics firms, enterprises managing large operational fleets, and transportation companies.

Why Choose Over Others

WEX is designed for travel heavy enterprises and operational businesses rather than just general SMB online purchases.

What Is a Virtual Card for Business?

A virtual credit card for business is a digitally issued payment card that can be used for online purchases, subscriptions, controlled vendor spending, and employee expenses. Unlike regular shared physical debit cards or credit cards, virtual options generate unique card details, including a dedicated number, expiration date, and CVV.

Businesses can use virtual debit cards and secured virtual credit products to improve spending control while also reducing fraud exposure from unauthorized purchases. Cards can then be assigned to one vendor, one employee, or one recurring service.

Unlike tools that are more consumer-focused, business virtual cards generally include admin controls, approval workflows, integrations with accounting software, and spending policies. Companies often use virtual cards to simplify expense tracking, reduce misuse of company funds, and manage subscriptions.

Types of Virtual Cards for Business

There are three main types of virtual cards for businesses to know about, each of which can be useful in their own ways.

Single-Use / Per-Transaction Virtual Cards

Single-use cards generate a unique card number for a single purchase or one single vendor interaction. These cards are ideal because they reduce fraud exposure during unfamiliar online transactions or contractor purchases. This approach is also ideal because it improves fraud prevention as stolen card information becomes useless once a single transaction is completed.

Recurring / Subscription Virtual Cards

We then have recurring cards which are designed for ongoing vendor payments, SaaS subscriptions, and more. Businesses are able to assign separate cards for each recurring service or software platform. This helps improve overall visibility across accounts payable, and also this makes cancellation much easier.

Employee-Issued Virtual Cards

We then have employee issued virtual cards, and these are tied directly to departments or individual team members. Finance teams can monitor employee spending, review transaction details in real time, and apply budgets. Many providers then also support digital wallet functionality through Google Pay and Apple Pay, which can be used for approved in store purchases.

Key Benefits of Virtual Cards for Businesses

There are several key benefits of virtual cards for businesses, including spend visibility, fraud containment, subscription and vendor control, and fast issuance and lifecycle management.

Spend Visibility

One of the main benefits of virtual cards is their visibility, as shared physical credit cards create confusion because multiple employees use the same payment source. However, with virtual cards, every vendor, employee, or subscription can get its own card.

This is great for expense management, and it gives finance teams a clearer view of business operations while also simplifying reconciliation. Businesses can then also identify waste more quickly, allowing for better recurring expense forecasting, which helps improve overall cash flow.

Fraud Containment

One of the next biggest benefits of virtual cards is fraud containment. With traditional plastic cards, businesses are at a major risk. If the single shared company card is compromised, every linked subscription and vendor may need updating.

On the other hand, virtual credit card and virtual debit systems reduce that exposure by isolating purchases into dedicated cards that have individual controls. Most platforms then also have enhanced security features, such as one time use cards, instant cancellation, merchant restrictions, and more, thus helping reduce unauthorized transactions.

Subscription/Vendor Control

Subscription sprawl is a growing finance problem for SMBs, where teams sign up for software, then forget about unused services.

This is why having multiple virtual cards for recurring software and specific vendors creates accountability, because finance teams are able to see exactly who owns each subscription and which department requested it.

This helps simplify cancellations as well, because instead of having to replace a company-wide credit card, admins can just deactivate the single isolated card. For SaaS-heavy organizations, this is a practical benefit of virtual payment infrastructure.

Fast Issuance and Lifecycle Management

The other main benefit of using virtual cards is that it is very quick. With physical cards, issuance can take days or even weeks. Virtual cards can be issued virtually instantly, and this is important for urgent purchasing, scaling teams, and remote hiring.

New employees are able to receive spending access right away without having to wait for plastic cards to arrive in the mail. When compared to traditional card systems, virtual issuance improves operational flexibility while helping businesses manage spend more efficiently.

Pros & Cons of Virtual Cards for Business

Pros

-

Better expense management and spending visibility

-

Faster issuance than physical credit cards

-

Stronger control over employee spending and subscriptions

-

Improved fraud containment through isolated card details

Cons

-

Some merchants still require a physical card

-

FX and funding fees may apply depending on provider

-

Not every provider supports international users without a US entity

-

Some virtual card transactions may trigger verification issues on older systems

Where Virtual Business Cards Are Accepted

The vast majority of modern virtual cards are widely accepted for cloud platforms, ad networks, contractor payments, SaaS subscriptions, and various standard online payments. With that being said, acceptance does vary depending on the issuing region and card structure.

For international operators, US issued products generally perform the best because many American merchants prioritize US BINs during fraud screening. That's just one reason why a secured Visa virtual credit card product, such as Halocard, often outperforms regional prepaid or debit-only alternatives. Thanks to featuring a US BIN and US billing address, Halocard has strong acceptance in the USA.

Frequently Asked Questions

What Are the Main Benefits of Virtual Cards for Businesses?

The biggest benefits of virtual cards for businesses include stronger fraud protection, better spending control, simplified reconciliation, and subscription management.

Can LLCs Get Virtual Debit Cards Without a Credit Card?

Yes, many providers will issue virtual debit cards that are tied directly to a business bank account for LLCs without requiring traditional underwriting.

Are Virtual Cards Better Than a Physical Card for Business Payments?

For many business payments, yes, virtual cards are better than physical cards because unlike physical cards, virtual options provide users with a stronger control system and easier cancellation management.

How Do Virtual Cards Help With Cash Flow?

Virtual cards help improve cash flow by improving visibility into recurring expenses, simplifying forecasting, and reducing subscription waste.

Can Virtual Cards Be Used for Business Travel?

Yes, many providers support business travel, employee meal expenses, and hotel bookings through mobile wallets and controlled virtual issuance.

Do Virtual Cards Work With Google Pay and Apple Pay?

Yes, many virtual card providers support Google Pay, Apple Pay, and other mobile wallets for various contactless payments and in store purchases.

How Many Virtual Cards Can a Business Create?

How many virtual cards a business can create depends on the provider, as some support only single cards, while some support dozens, and others even unlimited virtual cards, depending on the plan and structure.

Are Virtual Cards Good for Expense Management?

Yes, virtual cards are good for expense management, as they help improve reporting, reduce reconciliation, and provide spending controls for businesses.

What Is the Difference Between Virtual Debit and Virtual Credit Cards?

A virtual debit card generally draws directly from loaded funds or a bank account, whereas a virtual credit card uses credit authorization, similar to traditional issuers.

Can International Users Get Virtual Cards Without an SSN?

Yes, some providers, including Halocard, allow international users to get a virtual card without requiring a US Social Security Number.

Sources

-

Halocard. Instant, Private & Secure Virtual Cards | Halocard

-

Airwallex. Airwallex: Trusted Global Payments & Financial Platform

-

Airwallex. Plans & Pricing | Airwallex Official Site

-

Ramp. Spend Management, Corporate Cards & Accounts Payable Solutions | Ramp

-

Brex. Brex: The Modern Finance Software Platform | Spend Smarter

-

Extend. Pricing | Extend

-

Extend. Virtual credit cards & spend management for businesses | Extend

-

Multipass. What is a Virtual Card and Its Business Benefits | MultiPass

-

Concur. Getting the Most Out of Virtual Cards for Business | SAP Concur Canada

-

WEX. 7 advantages to virtual cards for your B2B payment needs | WEX Inc.

-

VENN. Virtual Cards: 10 Real Advantages & Drawbacks for Canadian Businesses

-

Float Financial. Top Five Use Cases for Virtual Cards in Canadian Businesses - Float

-

Airwallex. 10 Pros & Cons of Virtual Cards in 2024 | Airwallex CA

Sources checked on May 20, 2026.

*Please see Halocard's Terms of Service or Pricing for the most up to date pricing and fee information. This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Halocard LLC or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Halocard Virtual Cards

Instant approval

Create your first card in under 5 minutes.

Private purchases

Purchases never appear on your bank account.

Powered by Visa

Accepted at 175M+ merchants globally.

3 steps to create your virtual credit card

1. Sign-up with a phone

Sign up from your browser. No app download needed.

2. Quick identity check

Verify you're a real person in less than 3 minutes. No US residency required.

3. Add funds to your account

Use stablecoins, debit/credit card, or bank transfer (1%).

Your virtual card is ready.

That's it! Your virtual cards can now be used for online and in-person purchases anywhere in the world where Visa is accepted.