Best Virtual Credit Cards Bangladesh (2026)

Alison Becker

Editorial Team

-

This guide is for users in Bangladesh who need internationally accepted virtual cards, especially for online payments, subscriptions, and global digital services.

-

The main problem is that local bank cards are frequently declined on US merchants, due to regional BIN restrictions, bank controls, and limited international routing.

-

The top virtual card options in Bangladesh are Halocard, Upay, Wise, Mutual Trust Bank PLC, and Eastern Bank PLC, with Halocard being the best choice overall due to stronger US and global acceptance.

-

Thanks to its high acceptance rate in the US and globally, ease of access, and high level of security, Halocard is the best virtual card in Bangladesh.

Quick Overview Comparison

| Provider | Card Type (credit / debit / prepaid) | Fees | Funding | Limits | Acceptance | Best For |

|---|---|---|---|---|---|---|

| Halocard | Virtual credit (secured Visa) | Starting from 1,471.40 BDT/month or $12/month (25 cards); 1.5% FX on non-USD; 3.9% top-up via cards/wallets | Debit/credit card, Apple Pay, Google Pay, bank transfer (where supported) | No preset limit; spend only what you load; freeze / cap / pause controls | Very high, especially US and international websites | Bangladesh users paying US platforms, subscriptions, e commerce, SaaS, and global digital services |

| Upay (UCB Co-Branded) | Virtual prepaid card (Visa) | BDT 575 issue (incl. VAT); BDT 345/year renewal (may be waived with BDT 3,000 monthly spend); ATM: 0.8% + BDT 15 (NPSB), 1.8% international; FX mark-up ~2% | Free load from Upay app / agents; Upay wallet balance | Prepaid basis; per-txn BDT 10–50,000 (common services); monthly BDT 300,000 (typical wallet limits); yearly BDT 3,600,000 card limit | Strong in Bangladesh; mixed on US websites vs US-issued BINs | Local spending, bills, controlled online purchases, and occasional international transactions |

| Wise | Virtual debit card | No monthly fee; FX conversion typically 0.33%–0.7%; ATM after free allowance: $0.55 + 1.75% (plus operator fees) | Wise multi-currency balance (top up via supported methods in the app) | Limited to available balance; 2 free ATM withdrawals up to about $220/month then fees | Strong internationally; mixed on some US websites (debit routing/BIN rules) | Multi-currency spending, travel, low FX costs, international online purchases |

| Mutual Trust Bank PLC (MTB) | Virtual debit and virtual prepaid card | Virtual debit annual: BDT 250 ( | Virtual debit: MTB bank account balance. Virtual prepaid: load via MTB Smart Banking/app | Debit: limited to balance. Prepaid: limited to loaded amount; bank limits apply | Good locally; mixed abroad and on US merchants | MTB customers who want a bank-linked virtual card for local ecommerce and occasional international use |

| Eastern Bank PLC (EBL) | Virtual prepaid card (Visa/Mastercard/DCI/UPI) | Issuance: BDT 200 + VAT (~$1.80–$2.00 + VAT); PIN replacement free; other charges same as physical prepaid SOC (FX/currency conversion may apply) | Free fund loading from EBL CRM, branches, and SKYBANKING app | Max balance: BDT 1,500,000 (or USD equivalent); no ATM cash withdrawal support | Strong for local ecommerce/QR; international acceptance varies by merchant | App-based onboarding, controlled prepaid online shopping, QR payments, dual-currency use (BDT/USD) |

Currency conversion from BDT to USD accurate as of February 19, 2026.

Top 5 Virtual Cards in Bangladesh

The top virtual card options in Bangladesh are Halocard, Upay, Wise, Mutual Trust Bank PLC, and Eastern Bank PLC.

1. Halocard

Halocard is a US-issued Visa virtual credit card platform built for flexible and secure online payments. In Bangladesh, its biggest benefit is consistent acceptance on US and international websites that often reject locally-issued cards. Halocard focuses on providing cardholders fast access to virtual card numbers made specifically for secure online shopping and contactless purchases.

How It Works

Users in Bangladesh sign up with their phone number and email, followed by a quick verification process, allowing for near-instant card generation. Load funds onto the card using various funding methods and start shopping online, and add to Google Pay or Apple Pay to start making contactless payments.

Costs & Fees

-

Monthly fee: Starting from 1,471.40 BDT/month ($12/month) (up to 25 cards)

-

Creating a card: Included

-

Foreign exchange fee: 1.5% on non-USD transactions

-

Adding funds: 3.9% via card payments or wallets

Spending Limits & Usage Restrictions

There are no fixed spending limits. You can only spend what you load, and each card can be capped, paused, or frozen at any time. Halocard is built for online payments and digital wallets, not for withdrawing cash or using bank branches.

Key Advantages

-

Strong global acceptance with a US-issued Visa card

-

Fast setup without needing a Bangladeshi bank account

-

Multiple virtual card numbers for added privacy

-

Reliable for subscriptions, e commerce, and US platforms

-

Designed for international online use

Specific Drawbacks

-

Monthly subscription required

-

FX fees apply when paying in non-USD currencies

-

Not suitable for cash withdrawals or offline banking

Who It’s For

Halocard is for those in Bangladesh who pay US merchants or use international services and have had local bank cards declined in the past. It’s for freelancers, remote workers, online sellers, and individuals who want a virtual card separate from their main bank account with better acceptance abroad.

Why Choose Halocard Over Others

Halocard is often the best choice if acceptance on US websites is the priority. Because it uses US-based BINs on the Visa network, its cards are far more likely to be accepted by American merchants than a virtual debit card or a virtual prepaid card issued by Bangladeshi banks.

Compared to debit-based or prepaid card products from local providers, Halocard has faster setup, stronger international routing, and more control, so it’s a practical solution for global online spending from Bangladesh.

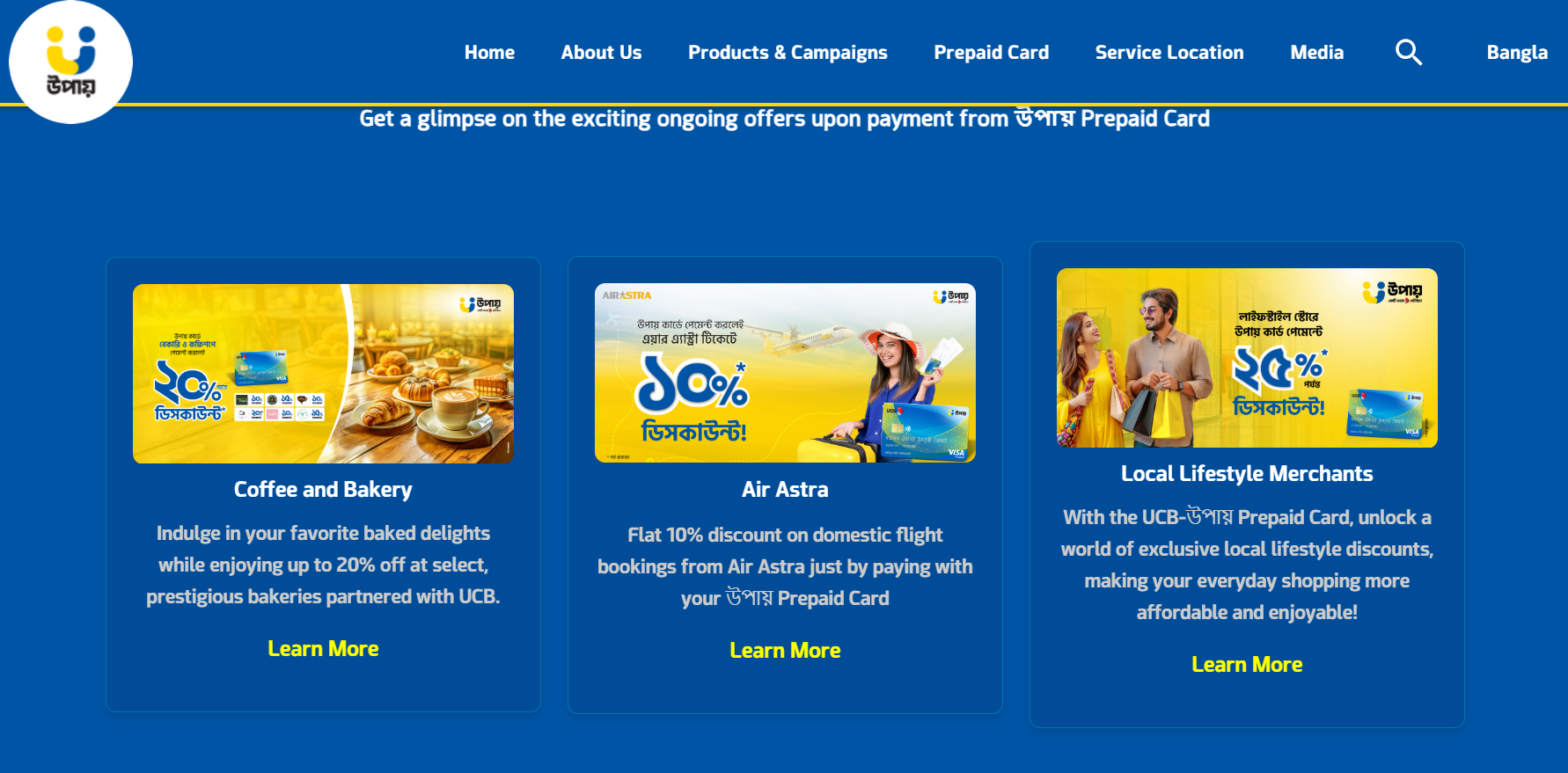

2. Upay

Upay has a UCB co-branded Visa virtual prepaid card designed for use in Bangladesh, with some support for foreign transactions. One of its biggest selling points is its easy accessibility, as users can pay directly through the Upay app. The card is closely tied to its other financial services - this is not a standalone virtual card platform.

How It Works

Users in Bangladesh need an active Upay account linked to their phone number. After completing the verification process, eligible applicant profiles can apply for the UCB–Upay prepaid card directly inside the app or through authorised agents. Once approved, the cardholder can then load funds and start spending immediately, with everything managed from the Upay app.

Costs & Fees

-

Card issuance fee: Commonly around BDT 575, including VAT, though promotions can reduce or waive this

-

Annual or renewal fee: Around BDT 345 per year (often waived if minimum monthly spending is met)

-

Loading funds: Free from Upay wallet or agents

-

Merchant payments (POS and online): Usually free

-

ATM withdrawal (local NPSB): Approximately 0.8% + BDT 15

-

ATM withdrawal (international): Approximately 1.8%

-

FX mark-up: Around 2% on foreign currency transactions

Exact charges can change, so users should always confirm current rates using the charge calculator in the Upay app.

Spending Limits & Usage Restrictions

Upay prepaid cards operate on a prepaid card basis, meaning spending is limited to the amount loaded. Transaction limits apply per transaction, daily, and monthly, depending on the activity.

Key Advantages

-

No traditional bank account required

-

Free load options through Upay wallet and agent network

-

Dual currency support for local and international use

-

Widely accepted across Bangladesh and at Visa merchants

-

Strong support for local bill payments and services

Specific Drawbacks

-

Issuance and annual fees may apply

-

FX mark-ups and international ATM charges increase costs

-

Acceptance can vary on some foreign ecommerce platforms

-

Prepaid structure limits flexibility compared to credit-based cards

Who It’s Best For

Upay is best for Bangladeshis who need a locally supported virtual prepaid card for everyday spending, bill payments, and occasional international transactions. It's suitable for those who want card access without having a separate bank account.

Why Someone Would Choose Upay Over The Others

Upay is often chosen for its convenience within Bangladesh, particularly thanks to its tight integration with local agents, bill payments, and mobile financial services.

3. Wise

Wise has a virtual debit card linked to a multi-currency account - ideal for low-cost online spending, international payments, and travel. For those in Bangladesh, Wise is generally used for paying abroad, making online purchases, and paying abroad. Wise is not a traditional bank, but operates as a regulated money services provider.

How It Works

Users can create a Wise account in the Wise app, complete identity verification, and then access a virtual card. In some cases, a physical card may be required before it is possible to get a virtual card. The virtual card can be used for making online purchases. Also, you can hold Bangladeshi Taka (BDT) or other currencies, and when you pay, the money is either spent directly from that balance or converted automatically at the mid-market rate.

Costs & Fees

-

Creating a digital card: Free

-

Monthly account fee: $0

-

Spending in a currency you hold: Free

-

Currency conversion fee: Typically 0.33%–0.7% per transaction (varies by currency pair)

Spending Limits & Usage Restrictions

Wise virtual debit cards can only spend the money available in your Wise balance. There are no preset credit limits.

Key Advantages

-

No monthly fees and a simple setup process

-

Mid-market exchange rates similar to Google’s rate

-

Strong security, including instant freeze and card replacement

-

Hold and spend money in 40+ currencies from one app

-

Very transparent pricing compared to many bank cards

Specific Drawbacks

-

Debit-based card, not a credit product

-

ATM fees apply after the free allowance

-

Some US merchants may decline debit virtual cards

-

Physical card may be required before full access

Who It’s Best For

Wise is ideal for customers in Bangladesh who frequently spend abroad or shop online in foreign currencies, and want to keep FX fees to a minimum.

Why Someone Would Choose Wise Over The Others

You would choose Wise if you're looking for predictable costs and fair exchange rate. It offers a cleaner fee structure for those making international purchases and managing multiple currencies, although acceptance can vary by merchant.

4. Mutual Trust Bank PLC

Mutual Trust Bank offers various virtual card options, including virtual debit card and virtual prepaid card products issued on Visa and Mastercard. These cards are designed mainly for Bangladesh-based users who want digital payments tied directly to a bank account, and are fully integrated into the MTB Neo and Smart Banking app, which means they work best for existing MTB customers.

How It Works

To get a virtual card, you must have an active MTC savings or current account, and use the MTB banking app. Eligible applicant profiles can apply digitally and receive the card details after completing the required verification process. Customers can use the virtual card for online purchases, QR-based merchant payments, ecommerce transactions, and supported ATM access through Cash by Code.

Costs & Fees

MTB charges differ depending on whether you choose a virtual debit card or virtual prepaid card. Based on published schedules and recent disclosures, typical fees include:

MTB Virtual Debit Card (Visa or Mastercard)

-

Annual fee: BDT 250 (≈ $2.30 USD)

-

Cash withdrawal at MTB ATMs: BDT 0 / $0 USD

-

Balance enquiry or mini statement: BDT 5 (≈ $0.05 USD)

MTB Virtual Prepaid Card

-

Annual fee (primary card): BDT 500 or $10 USD

-

Card replacement fee: BDT 300 (≈ $2.75 USD)

-

SMS alert fee: BDT 200 per year (≈ $1.80 USD)

-

FX mark-up on foreign currency spending: 3%

All fees may be subject to 15% VAT and can change over time, so users should always confirm current charges in the MTB app or the official Schedule of Charges.

Spending Limits & Usage Restrictions

MTB virtual debit cards spend directly from the linked bank account, while virtual prepaid cards can only spend the money you load in advance. Transaction limits apply per transaction, daily, monthly, and annually (depending on the card type).

Key Advantages

-

Issued by a regulated Bangladeshi bank

-

Available as both virtual debit card and virtual prepaid card options

-

Low annual fees compared to traditional credit cards

-

Integrated with MTB digital banking apps

-

Supports ecommerce, QR payments, and limited international use

Specific Drawbacks

-

Requires an active MTB bank account

-

Annual fees apply even for virtual-only cards

-

FX mark-up increases cost for foreign spending

-

Lower acceptance on some international and US platforms

-

Less flexible than standalone international virtual card services

Who It’s Best For

MTB virtual cards are best for Bangladesh-based customers who already use MTB banking services and want a simple virtual card for local use and occasional international spending.

Why Someone Would Choose MTB Over The Others

MTB is great for those who want to keep payments to a single banking system, with its local cards offering familiarity, local support, and clear fee structures, making them a practical choice for domestic digital payments.

5. Eastern Bank PLC

Eastern Bank PLC has various virtual prepaid cards offered through its SKYBANKING app. This is a fully online onboarding option, so you can get a virtual card without a pre-existing relationship with the bank. These are digital-only cards that support domestic and international payments, with many having dual-currency capabilities.

How It Works

Sign up through the EBL SKYBANKING app, complete onboarding, and apply for the specific card you want (Visa, Mastercard, DCI, or UPI options). Cards can be generated instantly inside the app, with full card details being accessible after setting a PIN.

Costs & Fees

-

Issuance fee: BDT 200 + VAT (Visa Daraz, Visa Lifestyle, Mastercard Aqua, Banglalink co-brand, DCI, UPI)

- USD equivalent: roughly $1.80–$2.00 + VAT (depends on exchange rate at the time)

-

PIN replacement: Free

EBL also states that all other charges follow the same Schedule of Charges as the equivalent physical card version. That commonly means:

-

Foreign currency conversion or FX charges may apply for international transactions

-

Other service fees can apply depending on transaction type

Because those “physical card” charges can change over time, the most accurate figures will be inside the SKYBANKING app or the latest Schedule of Charges on the EBL site.

Spending Limits & Usage Restrictions

EBL virtual prepaid cards run on a prepaid card basis. You load funds and can only spend what is available, so spending is never debited from a credit line. There is a maximum balance of BDT 1,500,000 (or USD equivalent) allowed on the card.

Key Advantages

-

Low issuance cost compared to many bank card products

-

Fully digital onboarding through the SKYBANKING app

-

No physical card, reducing loss and fraud risk

-

Dual currency option (BDT and USD) for approved international payments

-

Supports QR and ecommerce payments locally and abroad

Specific Drawbacks

-

Not ideal if you need cash, since ATM withdrawals are not supported

-

You may need passport endorsement for foreign transactions, depending on usage

-

“Other charges” depend on the physical card fee schedule, so costs are not fully fixed in one simple list

-

Requires required documents such as NID images and nominee details during the application process

Who It’s Best For

EBL virtual prepaid cards are best for Bangladesh-based customers who need a virtual prepaid card that they can easily generate for online shopping and controlled spending.

Why Someone Would Choose EBL Over The Others

EBL is a good fit for those who want a bank-issued virtual prepaid card with clear fees, easy onboarding, and dual currency support. It's also ideal for those who want a virtual card that can be easily managed from a single app.

What Is a Virtual Card?

A virtual card is a digital card, such as a digital debit card or credit card, that exist only online and are used for a variety of internet purchases, subscriptions, E commerce payments, and contactless payments.

Instead of getting a physical card, the cardholder receives card details inside of an app, including card number, expiry date, and security code.

For those in Bangladesh, a virtual card solves various problems. For one, many local bank card products face regional restrictions, with US platforms often rejecting non-US issued card numbers.

Also, virtual card usage improves security by keeping your main bank or card details hidden, thus reducing the risk when shopping online, along with tighter spending controls and faster access to global services without having to carry a physical card, visit branches, or handle cash.

Types of Virtual Cards

There are three main types of virtual cards; virtual debit cards, virtual credit cards, and virtual prepaid cards.

Virtual Prepaid Card

A virtual prepaid card is funded in advance. Here, you load money first and can then only spend whatever has been loaded onto the card. This prepaid card format limits risk and helps keep spending under control, although some virtual prepaid cards may have lower acceptance rates on some foreign store platforms.

Virtual Debit Card

Virtual debit cards are linked directly to a banking account, with payments being debited from the available money balance. These cards are common in Bangladesh, although acceptance abroad can at times be inconsistent.

Virtual Credit Card

A virtual credit card generally works like a regular credit card, but is issued digitally. These cards are often tied to credit limits and credit checks before customers can start spending.

However, certain virtual credit cards, like those from Halocard, are secured and not linked to a line of credit, making them easy to obtain. With just a few required documents for identity check, you can get a card instantly and start spending locally and internationally.

A benefit of virtual credit cards is that they generally have the highest acceptance rates on individual websites, especially where the US and other foreign countries around the world are concerned.

Benefits of Virtual Cards

Using virtual cards in Bangladesh has several benefits for cardholders looking for a smarter way to use their money.

Privacy and Security

A virtual card protects your main bank account or credit card details by masking those real details, and instead using the details from the virtual card. If a website is compromised, your primary information stays safe, plus, many card providers also allow you to freeze cards instantly.

Tighter Spending Controls

Virtual cards allow you to easily set limits, freeze cards, or create single-use numbers, thus allowing you to more easily manage your finances.

Online and Contactless Payments

A virtual card, although it is primarily built for online use, can also be added to digital wallets, such as Google Pay or Apple Pay, allowing for both online and contactless payments in store.

Increased Global Acceptance

Many virtual card providers, especially virtual credit card platforms that run on networks like Visa, such as Halocard, tend to have a high global acceptance rate. This is useful for those looking to make US and international purchases.

Pros and Cons of Virtual Cards in Bangladesh

Using a virtual card in Bangladesh comes with several advantages.

Pros

-

Better Security for Online Payments: Virtual cards significantly improve security when making internet purchases by masking primary card details. This reduces the risk of fraud for cardholders.

-

Easy to Freeze or Replace Instantly: Most virtual card providers allow you to freeze, delete, or replace a card directly from the app. This is ideal in the event that there is suspicious activity.

-

Ideal for Subscriptions and Digital Services: A virtual card works well for recurring services, SaaS tools, ads, and digital subscriptions. Managing all of your payments from one app is made easy.

-

No Physical Card Required: Once approved, users can get a card instantly, start spending within minutes, and make online payments without delays, paperwork, or delivery hassle. Not having a physical card also means that there is no plastic to be lost or stolen.

-

Better Acceptance on International Platforms: Many virtual card providers, especially virtual credit card providers, offer excellent acceptance on US and global platforms.

Cons

-

Acceptance Still Varies by Provider: Some virtual debit cards and prepaid cards, particularly those issued by a local bank, may be declined abroad.

-

Foreign Exchange and Funding Fees: Although it depends on the provider, spending in foreign currencies often incurs fees. Some cards may also charge fees to load money onto them.

-

Funding Limits and Delays: Certain prepaid options may have spending limits or loading limits. In some cases, loading may take time if verification or submission of documents is required.

-

KYC and Document Requirements: Most providers require documents such as a passport, proof of identity, and completed forms during the application process. Although this can slow down the application process, it does add to the security dimension.

-

Limited Use for Cash or Offline Needs: Although many virtual cards can be added to digital wallets for contactless payments, they are still limited in terms of being able to withdraw cash.

Frequently Asked Questions

Which Virtual Card Is Best in Bangladesh?

There are several good options in terms of the best virtual card in Bangladesh, with options such as Halocard being excellent for those who need broad acceptance on global and US platforms.

Can I Get a Free Virtual Card in Bangladesh?

Some bank apps in Bangladesh may offer free virtual cards, although they often have lower acceptance rates.

Does Wise Work in Bangladesh?

Wise does offer international transfers, but full virtual card issuance is limited for Bangladeshi applicant profiles.

What Is a Virtual Credit Card in Bangladesh?

A virtual credit card is a digital card issued online, typically by international providers rather than a local bank.

Can I Use a Bangladesh Virtual Card on US Websites?

Most options are declined, making US-issued virtual cards the better option.

Which Banks Offer Virtual Cards in Bangladesh?

Several banks in Bangladesh offer virtual cards, including, but not limited to, Eastern Bank (EBL), City Bank, Mutual Trust Bank (MTB), Midland Bank (MDB), and Dutch-Bangla Bank (DBBL).

Is a Virtual USD Card Available in Bangladesh?

Yes, but usually through international providers as opposed to domestic banks.

How Do I Instantly Get a Virtual Visa Card?

You can apply online, complete submission of documents, and receive a card instantly through providers like Halocard.

Are Virtual Cards Safe for International Shopping?

Yes. Virtual cards improve security, reduce fraud risk, and allow you to freeze access in real time.

Virtual Card Acceptance

Whether or not a virtual card is accepted depends on the issuing country and card type. Virtual credit card products generally have the highest acceptance rates when compared to virtual debit card and virtual prepaid card products. For example, issuers such as Halocard perform well because it uses US-issued Visa card numbers, allowing it to be consistently accepted abroad.

How to Get Halocard

For individuals in Bangladesh who want a dependable way to pay across international websites and digital platforms, Halocard offers a quick setup and a straightforward virtual card experience. You can create a card in minutes, add funds using supported options, and begin making secure online payments with strong global acceptance.

Steps

-

Create Your Account

Sign up using your email or phone number and complete a short verification to activate access. -

Generate Your Virtual Card

Issue a virtual card instantly from the dashboard, ready for secure international transactions. -

Add Funds

Load money using available funding methods and control how much the card can spend. -

Start Paying Online

Use your card immediately for global websites, subscriptions, digital services, and US-based merchants.

Why Halocard Stands Out

-

High acceptance across US and international platforms

-

Built specifically for cross-border online payments

-

Fewer transaction declines than many local bank cards

-

Reliable routing for subscriptions, shopping, and digital services

-

Secure controls for everyday online spending

If you need a virtual card that performs consistently for international, online, and secure payments from Bangladesh, Halocard is a simple place to begin.

Sources

-

Mutual Trust Bank. upay | উপায় Sourced on February 12, 2026.

-

Wise. Virtual Card | Create your virtual Wise Multi-Currency Card - Wise Sourced on February 12, 2026.

-

Mutual Trust Bank. Schedule of Charges - Mutual Trust Bank PLC Sourced on February 12, 2026.

-

Mutual Trust Bank.Schedule-of-Charge-MTB-Cards-dec23.pdf Sourced on February 12, 2026.

-

Mutual Trust Bank.MTB Prepaid Cards Sourced on February 12, 2026.

-

Mutual Trust Bank. Debit Card - Mutual Trust Bank PLC Sourced on February 12, 2026.

-

Mutual Trust Bank. Mastercard Virtual Debit Card - Mutual Trust Bank PLC Sourced on February 12, 2026.

-

Mutual Trust Bank. Virtual Prepaid Card - Mutual Trust Bank PLC Sourced on February 12, 2026.

-

Eastern Bank PLC. Eastern Bank PLC. | EBL Virtual Prepaid Card Sourced on February 12, 2026.

-

Eastern Bank PLC. EBL-Virtual-Prepaid-Card-FAQ-External.pdf Sourced on February 12, 2026.

Halocard Virtual Cards

Instant approval

Create your first card in under 5 minutes.

Private purchases

Purchases never appear on your bank account.

Powered by Visa

Accepted at 150M+ merchants globally.

How to get a virtual credit card in 3 simple steps

1. Sign-up with your phone

Sign up from your browser. No app download needed.

2. Complete a quick identity check

Verify you're a real person. No SSN or US residency required.

3. Add funds to your account

Use stablecoins, debit/credit card or ACH/SWIFT bank transfer (coming soon).

Your virtual card is ready.

That's it! Your virtual cards can now be used for online and in-person purchases anywhere in the world where Visa is accepted.